FINANCIAL REVIEW

Consolidated Net Debt of ex-Infrastructure project companies

*Non-IFRS financial measure. For the definition and reconciliation to the most comparable IFRS measure, see Alternative Performance Measures annex in the Integrated Annual Report (page 269) **Other from ex-infrastructure project companies includes non-current restricted cash, forwards hedging and cross currency swaps balances, intragroup position balances and other short term financial assets, as explained under section 2.1 (Consolidated Net Debt) of the Alternative Performance Measures. ***Other from infrastructure project companies includes short and long term borrowings, non current restricted cash and intragroup position balances, as explained under section 2.1 (Consolidated Net Debt) of the Alternative Performance Measures.

*Non-IFRS financial measure. For the definition and reconciliation to the most comparable IFRS measure, see Alternative Performance Measures annex in the Integrated Annual Report (page 269) **Other from ex-infrastructure project companies includes non-current restricted cash, forwards hedging and cross currency swaps balances, intragroup position balances and other short term financial assets, as explained under section 2.1 (Consolidated Net Debt) of the Alternative Performance Measures. ***Other from infrastructure project companies includes short and long term borrowings, non current restricted cash and intragroup position balances, as explained under section 2.1 (Consolidated Net Debt) of the Alternative Performance Measures.

(*) In 2026, ex-infrastructure debt includes outstanding ECP (Euro Commercial Paper), which at December 31st, 2025, had a carrying amount of EUR 100 million (2.040% average rate) and maturing in 2026.

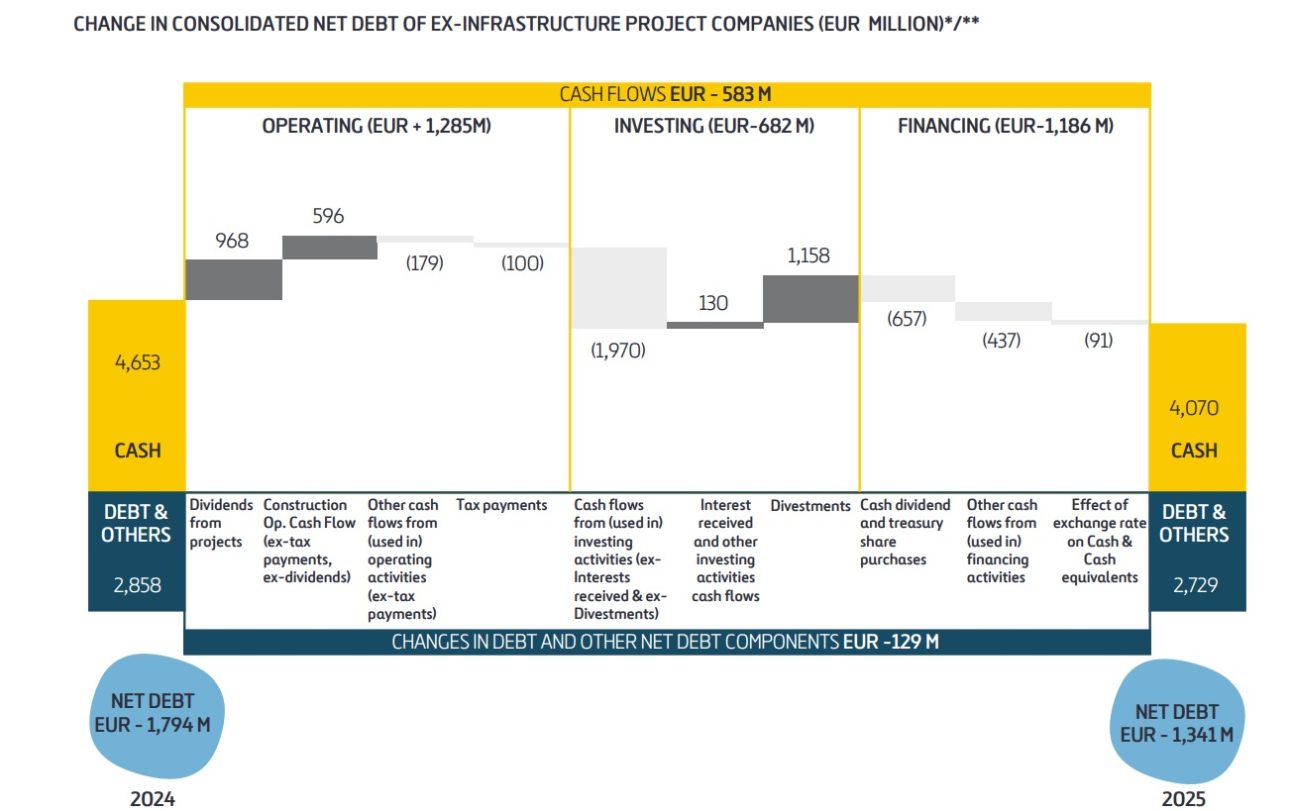

CHANGE IN CONSOLIDATED NET DEBT OF EX-INFRASTRUCTURE PROJECT COMPANIES (EUR MILLION)*/**

-

(**) Due to rounding, numbers may not add up precisely.

Ferrovial’s consolidated net debt includes Budimex’s consolidated net debt at 100% that reached EUR -733 million in December 2024 and EUR -655 million in December 2025.

Cash and cash equivalents at ex-infrastructure project companies stood at EUR 4,070 million in December 2025 vs. EUR 4,653 million in December 2024. The main drivers of this change were:

- Dividends from projects amounted to EUR 968 million, of this amount EUR 880 million came from Highways including EUR 452 million from 407 ETR, EUR 281 million from Texas Managed Lanes, EUR 89 million from I-66 and EUR 33 million from I-77. Additionally, Energy distributed EUR 54 million corresponding to the return of capital invested in a photovoltaic plant in Texas. The Airports division distributed EUR 30 million, including EUR 16 million from Heathrow, EUR 7 million from Dalaman and EUR 7 million from Doha’s airport maintenance contract.

- Construction operating cash flow (ex- tax payments, ex-dividend) reached EUR 596 million, posted a solid uplift, driven by Q4 working capital seasonality in Poland and Spain, and further enhanced by pre-payments and compensations received in the US and Canada.

- Tax payments reached EUR -100 million, including EUR 47 million of corporate income tax in Budimex.

- Investments totaled EUR -1,970 million, mainly due to the additional 5.06% stake acquired in 407 ETR (EUR 1,271 million), the EUR 236 million of equity invested in NTO, and the acquisition of the Milano Solar project for EUR 17 million.

- Interest received and other investing activities cash flow amounted to EUR 130 million, mainly related to cash remuneration.

- Divestments reached EUR 1,158 million, largely driven by the divestment of Heathrow (EUR 539 million) and the divestment of AGS (EUR 533 million), along with the sale of the mining services business in Chile for EUR 24 million and the deferred payment for the sale of Serveo of EUR 15 million.

- Cash dividend and treasury share purchases at EUR -657 million in 2025, (EUR -831 million in 2024), including EUR -156 million from the cash dividend and EUR -501 million of share repurchases.

Following Market standards, dividends declared (EUR-626million in 2025) are based on the share price at the time of delivery to shareholders. This amount may differ from the cash flow statement, as treasury shares related to the scrip dividend are purchased at the share price prevailing at each transaction, whereas the amount distributed to shareholders under our scrip dividend programs is calculated based on the share price at the time of delivery. For further details on each of the scrip dividend programs of 2025, please refer to Appendix I. - Other cash flows from (used in) financing activities amounted to EUR -437 million, including the repayment of the revolving facility (EUR -250 million), the reduction of Euro Commercial Paper (EUR -200 million), financial leases (EUR -121 million), dividend to minorities (EUR -77 million) and interest payments (EUR -64 million), partially offset by the convertible bond issuance (EUR 350 million).

- Effect of exchange rate on Cash & Cash equivalents was EUR -91 million, mainly from USD. As of December 2025, Ferrovial has notional foreign exchange hedges amounting to 2,847 million in USD and 538 million in CAD, with corresponding mark-to-market values of EUR 140 million and EUR 7 million, respectively (total of EUR 147 million). These amounts are not included in the net cash position.

*Non-IFRS financial measure. For the definition and reconciliation to the most comparable IFRS measure, see Alternative Performance Measures annex in the Integrated Annual Report (page269).