BUSINESS LINES

Construction

Revenue increased by +7.5% LfL vs. 2024, with significant growth seen in North America at +11%. North America contributed 35% to revenue, while Poland accounted for 29%.

In 2025, Construction recorded an adjusted EBIT of EUR 352 million, resulting in a 4.6% adjusted EBIT margin (3.9% in 2024). The division has improved very positively across all subdivisions compared to previous quarters, outperforming the strategic long-term average target.

Details by subdivision:

- Budimex: Revenue increased by +4.4% LfL vs. 2024, primarily attributable to a strong performance in Building Construction Works contracts as well as Service division. The adjusted EBIT margin in 2025 stood at 9.2%, above the 8.0% in 2024. Q4 exceeded average profitability driven by one-off impact of relevant contract amendments under long term agreements, combined with higher contribution from late-stage contracts, where residual risks have been successfully mitigated. The Building segment stood out in particular, having implemented a selective bidding strategy and capitalized on opportunities in military contracts and the Polish Deal program. In addition, the solid performance of the Steel Structures and Road Maintenance businesses contributed positively, together with the momentum generated by the completion of the design phase in several Civil Works projects, which has enabled significant progress in their execution.

- Webber: Revenue increased by +21.1% LfL vs. 2024, largely driven by the execution of Civil Works projects, on the back of higher level of contract awards in recent years. The adjusted EBIT margin stood at 3.2% in 2025, above the 3.0% achieved in 2024.

- Ferrovial Construction: Revenue grew by +2.8% LfL vs. 2024, primarily due to a higher contribution from Canada and Spain, partially offset by the completion of major contracts in the United States, such as the California High‑Speed Rail project and the Silvertown Tunnel in the United Kingdom.

The adjusted EBIT margin was 2.4% in 2025 (1.8% in 2024) continuing the positive trend seen in previous quarters. This performance was supported by broad-based improvements across all regions, resulting from effective risk mitigation in the final phases of projects and improved execution as projects advanced beyond their initial stages. Profitability in 2025 was also affected by significant investment effort in bidding for projects in USA in the coming years, as well as by costs related to digitalization and IT systems.

2025 ORDER BOOK & LFL CHANGE VS 2024: (EUR million)

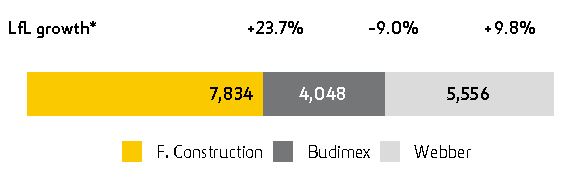

The order book reached at a record-high level of EUR 17,438 million as of December 2025 (+10.1% LfL compared with December 2024). The Civil Works segment remains the largest segment (69%) and continues to adopt highly selective criteria when participating in tenders. North America accounted for 46% of the order book, followed by Poland with 22%.

The percentage of the construction order book (excluding Webber and Budimex) from projects with Ferrovial reached 4% in December 2025 (6% in December 2024).

As of December 2025, the order book figure does not include pre-awarded contracts or contracts pending of commercial or financial close, amounting to approximately EUR 2.5 billion. These primarily consist of contracts from Budimex (EUR 1,755 million) and in Ferrovial Construction (EUR 750 million) related to the Anillo Vial Periferico project in Peru.

P&L DETAILS (EUR million)

| CONSTRUCTION | Q4 25 | Q4 24 | VAR. | FY 25 | FY 24 | VAR. | LfL growth* |

|---|---|---|---|---|---|---|---|

| Revenue | 2,233 | 1,999 | 11.7 % | 7,653 | 7,236 | 5.8 % | 7.5 % |

| Adjusted EBITDA* | 200 | 106 | 87.8 % | 511 | 430 | 18.8 % | 19.9 % |

| Adjusted EBITDA margin* | 8.9 % | 5.3 % | 6.7 % | 5.9 % | |||

| Adjusted EBIT* | 150 | 81 | 84.9 % | 352 | 284 | 24.0 % | 24.2 % |

| Adjusted EBIT margin* | 6.7 % | 4.1 % | 4.6 % | 3.9 % | |||

| Order book*/** | 17,438 | 16,755 | 4.1 % | 10.1 % |

*Non-IFRS financial measure. For the definition and reconciliation to the most comparable IFRS measure, see Alternative Performance Measures in the Integrated Annual Report (page 269)**Order book vs. December 2024.

| BUDIMEX | Q4 25 | Q4 24 | VAR. | FY 25 | FY 24 | VAR. | LfL growth* |

|---|---|---|---|---|---|---|---|

| Revenue | 718 | 607 | 18.4 % | 2,246 | 2,119 | 6.0 % | 4.4 % |

| Adjusted EBITDA* | 104 | 63 | 65.8 % | 251 | 207 | 21.3 % | 19.4 % |

| Adjusted EBITDA margin* | 14.4 % | 10.3 % | 11.2 % | 9.8 % | |||

| Adjusted EBIT* | 90 | 53 | 69.9 % | 206 | 170 | 21.2 % | 19.3 % |

| Adjusted EBIT margin* | 12.5 % | 8.7 % | 9.2 % | 8.0 % | |||

| Order book*/** | 4,048 | 4,389 | -7.8 % | -9.0 % |

*Non-IFRS financial measure. For the definition and reconciliation to the most comparable IFRS measure, see Alternative Performance Measures in the Integrated Annual Report (page 269)**Order book vs. December 2024.

| WEBBER | Q4 25 | Q4 24 | VAR. | FY 25 | FY 24 | VAR. | LfL growth* |

|---|---|---|---|---|---|---|---|

| Revenue | 574 | 515 | 11.6 % | 1,997 | 1,725 | 15.8 % | 21.1 % |

| Adjusted EBITDA* | 36 | 19 | 94.1 % | 119 | 100 | 19.2 % | 24.4 % |

| Adjusted EBITDA margin* | 6.3 % | 3.6 % | 6.0 % | 5.8 % | |||

| Adjusted EBIT* | 20 | 15 | 34.3 % | 63 | 52 | 21.0 % | 25.9 % |

| Adjusted EBIT margin* | 3.6 % | 3.0 % | 3.2 % | 3.0 % | |||

| Order book*/** | 5,556 | 5,710 | -2.7 % | 9.8 % |

*Non-IFRS financial measure. For the definition and reconciliation to the most comparable IFRS measure, see Alternative Performance Measures in the Integrated Annual Report (page 269)**Order book vs. December 2024.

| F. CONSTRUCTION | Q4 25 | Q4 24 | VAR. | FY 25 | FY 24 | VAR. | LfL growth* |

|---|---|---|---|---|---|---|---|

| Revenue | 940 | 877 | 7.1 % | 3,409 | 3,392 | 0.5 % | 2.8 % |

| Adjusted EBITDA* | 60 | 25 | 138.3 % | 141 | 123 | 14.2 % | 17.1 % |

| Adjusted EBITDA margin* | 6.3 % | 2.8 % | 4.1 % | 3.6 % | |||

| Adjusted EBIT* | 40 | 13 | 204.1 % | 82 | 61 | 34.3 % | 36.9 % |

| Adjusted EBIT margin* | 4.2 % | 1.5 % | 2.4 % | 1.8 % | |||

| Order book*/** | 7,834 | 6,657 | 17.7 % | 23.7 % |

*Non-IFRS financial measure. For the definition and reconciliation to the most comparable IFRS measure, see Alternative Performance Measures annex in the Integrated Annual Report (page 269)**Order book vs. December 2024.